Vega is the option greek that measures an option’s sensitivity to changes in implied volatility. As an option seller, understanding Vega is crucial because it directly impacts your exposure to market uncertainty and can significantly influence your PnL.

Key Takeaways

- Vega Explained: Vega measures an option’s sensitivity to changes in implied volatility, reflecting the expected future volatility of the underlying asset. When you sell options you are short vega, meaning that if implied volatility decreases you make money. Conversely, if implied volatility increases you lose money.

- Characteristics of Vega: Vega is highest for at-the-money options and increases with the time to expiration, making long-term, at-the-money options the most sensitive to volatility changes.

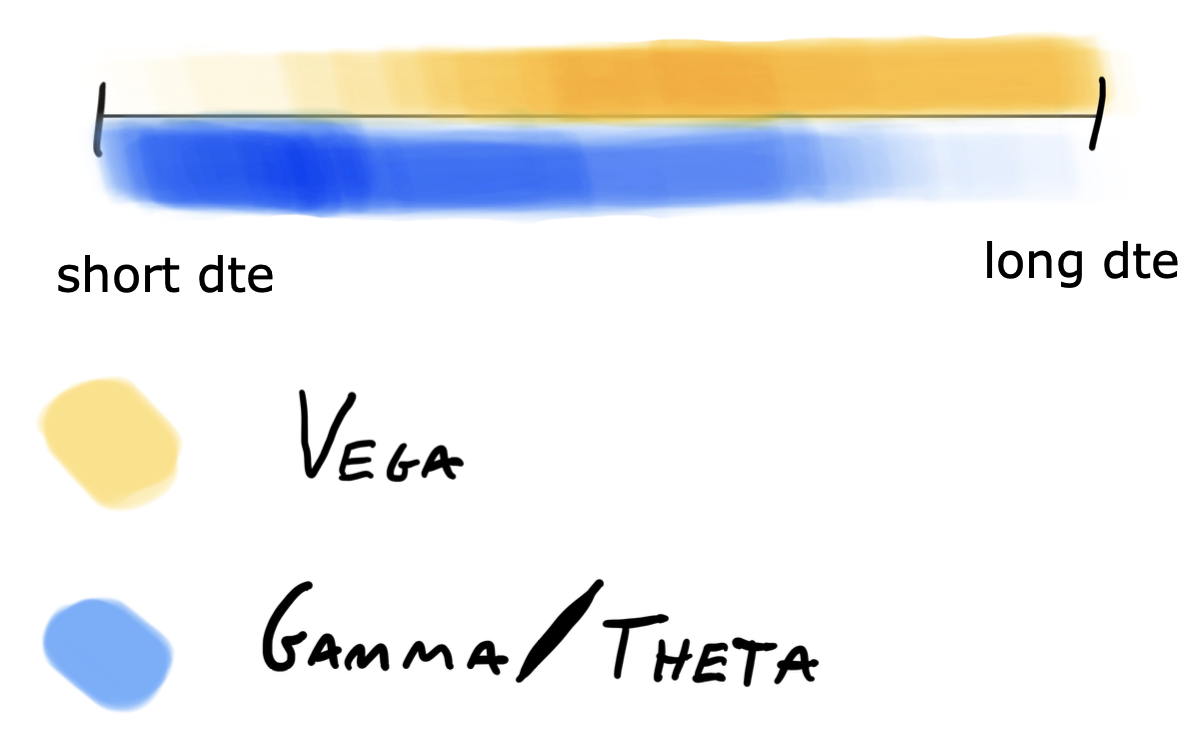

- Strategic Application: When you are trading longer dated options, your PnL will be influenced more by changes in perception about the future rather than the day to day movement of the underlying stock. When you are trading shorter dated options, your PnL will be influenced more by the day to day movement of the underlying stock rather than changes in perception of how much it will move in the future.

Click here for an overview of all the option greeks

What is Vega?

Vega represents the amount by which the price of an option changes in response to a 1% change in the implied volatility of the underlying asset. In simpler terms, Vega quantifies your exposure to fluctuations in market uncertainty.

The Role of Implied Volatility

Implied volatility reflects the market’s expectations for future volatility of the underlying asset. When implied volatility increases, it indicates that the market anticipates greater price fluctuations, leading to higher option premiums. Conversely, when implied volatility decreases, it suggests lower expected price movements, resulting in lower option premiums.

Practical Example: Vega in Action

Let’s illustrate Vega with a practical example involving Apple (AAPL):

- Current Price: AAPL is trading at $200.

- Vega: The 200 call option has a Vega of 1.0.

If AAPL’s implied volatility is currently 30% and the market suddenly anticipates a terrible quarter for Apple, causing implied volatility to spike to 40%, the impact on the 200 call option would be as follows:

- Change in Implied Volatility: 40% – 30% = 10%

- Change in Option Price: Vega (1.0) * Change in IV (10%) = $10

So, if you initially bought the 200 call option for $15, its new price would be $15 + $10 = $25, reflecting the increased market uncertainty.

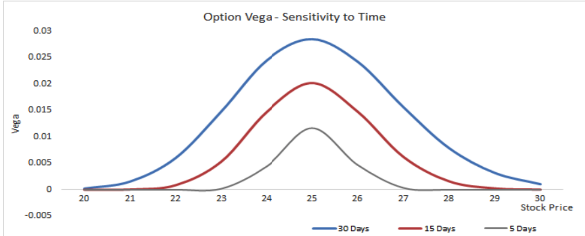

Understanding Vega’s Characteristics

1. Highest at the Money

Vega is highest for at-the-money options. This means options whose strike prices are closest to the current price of the underlying asset have the highest sensitivity to changes in implied volatility.

2. Increases with Time

Unlike Gamma and Theta, which decrease with time, Vega increases with the time to expiration. Long-dated options have higher Vega, making them more sensitive to changes in implied volatility compared to short-dated options.

Here’s what these characteristics actually look like:

As you can see, Vega starts low for short-term options and increases significantly for long-term options.

How to Consider Vega In Your Strategies

Depending on the opportunity you are analyzing, vega may or may not be the greek that you want the most exposure to.

For example, if your view is that a stock is going to move less than implied over the next 10 days, your vega exposure does not matter very much. What you really want to be doing is maximizing your exposure to the difference between implied and realized volatility.

To do this, you will structure your trade in a way that has more exposure to theta and gamma. For example you might sell an at-the-money straddle with 10 days to expiration.

But let’s say you look at another opportunity and this time your view is that the level of implied volatility is too high. Maybe there has been some panic recently and the market is implying that the stock is going to be seeing some massive swings for the next 6 months. If you think the market will become more rational and the level of implied volatility will come down, this is a situation where you want to maximize your exposure to the level of implied volatility and actually minimize your exposure to today’s implied VS realized volatility.

In this case, you would want to sell an at-the-money 180 DTE straddle because it would have the most vega and least gamma/theta exposure.

Here is an example of what the term structure may look like in this scenario. As you can see, every single expiration has an elevated implied volatility, pushing close to the highest we have seen. It’s in situations like this where the opportunity can be found in these further dated expirations.

Conclusion

Some of the best trades I’ve ever taken have been vega oriented. Understanding this exposure gave me a new perspective on how volatility can be monetized and it’s always something I look at when analyzing unique trading situations. Hopefully after reading this article you have a few ideas to explore and a newfound appreciation for how changes in implied volatility impact your option selling strategies!