One of the things that makes options such an attractive asset to trade is that there are so many dimensions to them. They can be used to express almost any view you have. But how do we actually describe these different dimensions? This is where the option greeks come into play.

The Greeks represent different dimensions of risk associated with taking an options position. They help us take advantage of the risks we want and remove the risks we don’t want. Simply put, we need to know them.

This article is a complete guide on everything you need to know about Delta, Gamma, Theta, and Vega – the four core option greeks.

Key Takeaways

- Greeks Describe Your Risk Exposures: When you place an option trade, your PnL can change for a number of reasons. Depending on the structure you trade, these reasons can be different. Option Greeks tell you what exposures your position is carrying so you can be sure that your trade is expressing your view on the market correctly.

- Understanding Delta, Gamma, Theta, and Vega: Delta measures price sensitivity to the underlying asset, Gamma reflects changes in Delta, Theta represents time decay, and Vega gauges sensitivity to volatility changes. These Greeks are crucial for managing option risks and crafting strategies.

- Applying the Greeks in Trading: Use Delta-neutral strategies to mitigate directional risk, monitor Gamma to manage rapid Delta changes, capitalize on Theta decay for income, and leverage Vega to profit from volatility changes.

- Professional Edge: Mastering the Greeks provides a competitive edge, enabling traders to develop informed strategies that maximize profits and minimize risks, essential for successful option selling.

Part 1: What Do I Mean By Risk?

When we talk about option greeks the word risk is going to come up very often. But I do not mean risk in the traditional sense, where it has a negative connotation. I do not mean risk as in “This is risky”.

When I use the word risk, I am talking about exposure.

For example, when you buy a stock, you have exposure to how the share price changes. For every dollar increase in share price, you make a dollar. For every dollar decrease, you lose a dollar.

With options there are many different exposures that you have the option to get exposure to. And there will be risks that you perhaps do not want exposure to. All of these are described to us through the option greeks. When you put on a trade, you are trying to express a particular view, and with that particular view, comes a particular risk exposure that you will want.

For example, “I think that options are expensive”.

Means that “I want exposure to the difference between implied and realized volatility”

Which means that your position should have theta and gamma exposure, but maybe not delta. (these are the Greeks we are talking about, they will make sense to you shortly).

When you understand the Greeks, you understand your risk exposures because they provide a framework to quantify them.

When you understand your risk exposures, you are able to ensure that the trade you place is articulating your view of the market correctly.

You Need to Understand Your Tools If You Want To Make Money

There’s no way around it. Options are complex financial instruments, and they are sensitive to various factors beyond the underlying asset’s price movements. While stock prices move linearly, options exhibit more intricate behavior due to their multidimensional nature.

Imagine if you hired an electrician to install wiring in the house you are building. Imagine he showed up to your house and told you that he doesn’t know how his hammer and drill work.

You would fire him instantly. It’s an assumption that a professional knows how their tools work.

Part 2: The Comprehensive Overview of The Greeks

By understanding option Greeks we can take advantage of the risks we want and remove the risks we don’t want. It is important to remember, Greeks are not an edge. They simply describe our current exposures (risks). We will cover the Greeks so we can understand how an option changes and why we make money or lose money. We will be covering; Delta, Gamma, Theta, Vega.

Keep in mind, Greeks (our current risks) change. They are dynamic and should not be thought of as stagnant.

1. Delta

Delta Measures how much the option’s price will change for each 1-point move in the underlying stock. So, a call option with a delta of 0.25, or 25%, indicates the option will gain 25 cents for every one dollar the underlying stock gains. Calls have positive deltas, since they gain in value as the stock rises, while puts have negative deltas, as these contracts will lose value as the stock rises.

We call trading stock, “Delta-one”. When we own shares we have a delta of 1. If we own 1 share of AAPL and it goes up $1, we make $1. If we own 1000 shares of AAPL, then we have a delta of 1000 meaning that if AAPL goes up by $1, we make $1000.

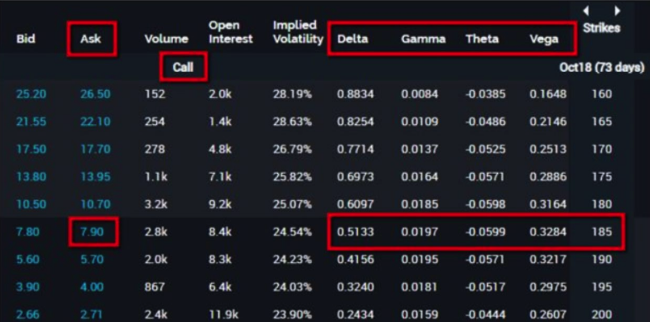

When we look at an option chain, we will notice that options at different strike prices have different deltas.

Notice how each call has a different delta at a different strike price. With .30 delta, our option price increases by 30 cents for each $1 move the stock gains and our instantaneous PnL would be $30 since each contract holds a value of 100 shares.

For puts, our options will have negative deltas. A put option with a -.70 delta would lose 70 cents in value for every $1 that the stock gains. Our instantaneous PnL for a single dollar change in the stock price in this situation would be -$70 since -.70 x 100 = -$70.

One factor to note is that across the option chain the difference between the call delta and the put delta has to equal to 1. For an option with the strike of $100, if the call has .6 delta, then the put will have -.4 delta (.6 – (-.4) = 1). Also note that the delta of an option is similar to the probability of an option expiring in the money. For example an option with a delta of .50 has a 50/50 chance of expiring in the money. This is why you will see OTM options trading with a low delta while an ITM option with a high delta.

To read more about delta click here

2. Theta

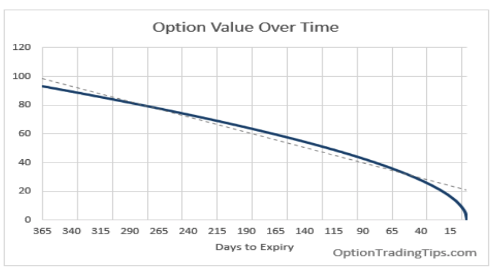

Theta gauges the time value of an option. Theta defines the loss in value an option will experience as time passes, and it’s usually expressed on a per-day basis.

Buying premium will result in a negative theta, because time is working against you, while selling premium involves a positive theta, since the passage of time works in your favor. Think about theta as the rent you collect for selling that option. However, as you will see later, this rent does not come for free.

So, a long option with a theta of -0.10 will lose about 10 cents per day in value, assuming the stock price and volatility are constant.

Theta is non-linear, because it accelerates as the option gets closer to expiration. This rate of decay is proportional to the square root of the time remaining before expiration.

Theta is the inverse of gamma. When you buy gamma, you are paying out theta every single day. In trading there is a saying “One man’s theta is another man’s gamma”. Theta gains will offset your gamma losses if implied volatility is greater than realized volatility. If the move is smaller than implied, then the theta will outweigh the gamma. In this case, being short on the option pays out.

To read more about theta click here

3. Gamma

Gamma is a second-order derivative, as it reflects the unit change in the delta for each 1- point change in the price of the underlying stock. It is your sensitivity to the quick movements of the underlying.

If you are long Gamma and you own the option, then any quick movement will benefit you as the buyer. When you are expecting a big movement on a stock then you want more exposure to Gamma, because if you do get a quick movement then you will get paid out alot, but if you don’t get quick movement then you will not get paid out.

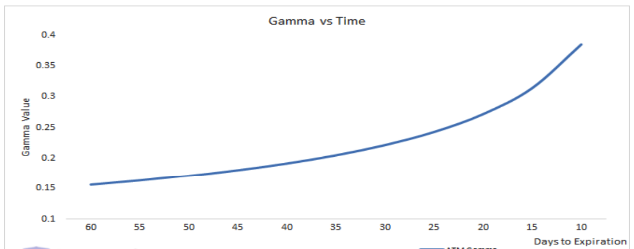

- Gamma is higher the closer we get to expiration and lower the further we are from expiration.

- Gamma is highest at the money and is lower the further we are out of the money.

To read more about gamma click here

4. Vega

Vega measures the change in the option price relative to a change in the option’s implied volatility, and it’s expressed in dollar terms.

An option with a Vega of 0.25 will change by 25 cents for every percentage-point change in the implied volatility. Long calls and puts have positive Vega, while short calls and puts have negative Vega.

These volatility changes are not absolute, though — they’ll have a lesser impact on the price of longer-term options, as well as far out-of-the-money or deep in-the-money options, and options with little time until expiration measures the sensitivity of an option’s price to changes in the volatility of the underlying asset. It indicates how much an option’s price will change for a 1% change in implied volatility.

For example, an AAPL $200-strike option is trading for $10 with a Vega of 1.00 with IV at 30. If IV moves from 30 to 40, then vega will raise the value of the option by the amount IV moved multiplied by how much vega the option has. In this case, IV raised by 10 so vega will raise the price of the option to $20 since 1.00 x 10 = 10.

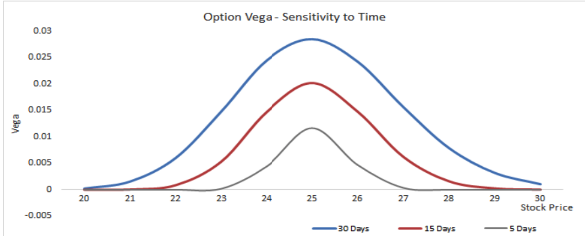

- Vega is highest at the money and lower out of the money.

- Vega increases with time.

- If you think uncertainty will increase then you want to buy the far dated options because they are the most sensitive to Vega and vice versa

To read more about Vega click here

Part 3: Applying the Greeks in Option Selling

Understanding the Greeks allows traders to dissect the complexities of options and develop robust selling strategies. Here’s how the Greeks can be applied in various option-selling scenarios:

Delta-Neutral Strategies

Delta-neutral strategies aim to eliminate the directional risk associated with the underlying asset. By balancing positive and negative Delta positions, traders can create a portfolio that remains relatively stable regardless of price movements in the underlying asset.

- Example: A trader thinks that 30 day implied volatility is going to be higher than realized volatility. They have no view on direction. They sell an at the money straddle, which has the following exposures.

- Delta neutral

- Long theta

- Short gamma

- Short vega

The trader plans to delta hedge this position daily in order to maintain the delta neutral exposure even as the stock price begins to drift around.

Trading The Change In Implied Volatility

As the markets opinion about how much a stock will move in the future changes, the level of implied volatility also changes. Vega is the greek that describes you exposure to changes in implied volatility, and as such, it is something you can actually trade!

- Example: XYZ company recently came out with some really bad news related to one of their products. The stock dropped 10% when the news was released and has since stabilized. You notice that the implied volatility across the term structure has not come down. You decide to sell an at the money straddle with 180DTE. The structure you chose has the following exposures

- Delta neutral

- Long theta (very little)

- Short gamma (very little)

- Short vega (a lot)

This position will not change very much on a day to day basis unless there is a shift in implied volatility. By going further out in time, you created a structure where you have very little exposure to direction and the day to day movements of the stock. But you have a lot of exposure to changes in implied volatility, which is exactly what you were looking for!

An Exercise To Help You Master The Greeks

After reading this article you have pretty much all the theoretical knowledge that you need. The next step in the learning process of understanding the greeks is to actually place a trade.

The way that I did this was by writing out my idea on a piece of paper and translating my opinion into option greeks. For example, if I wrote “I think implied volatility will be higher than realized volatility over the next 10 days, and I don’t care which direction the stock trends” Then I would translate that into greeks. “Delta neutral, long theta, short gamma, short vega”.

The last step would be to create a list of the structures that reasonably give me this exposure. “Short straddles and short strangles give me this exposure.” and from there I would pick between the two.

Mastering the Greeks is essential for anyone serious about option selling. We need to understand Delta, Gamma, Theta, and Vega, in order to express our views on the market correctly.

There is literally nothing worse than being right and not getting paid. So make sure you understand how to set your trades up such that they express your view correctly.